You’ve heard the numbers: 690, 740, 805. Three simple digits that can seem mysterious, abstract, or both. However, in the real world, your credit score largely determines what type and how much credit you can obtain, what interest rates you’ll pay — and, sometimes, whether you’ll land that great new job you desire.

Do we have your attention now? Thought so.

Understanding how the big three credit bureaus (Experian, Equifax, and TransUnion) calculate your credit score is key to learning how to proactively manage your credit and safeguard your all-important three digit credit score.

Your score allows businesses to assess your ability to repay money you borrow. Checking your credit score, and taking steps to improve it if necessary, are key steps in buying a new home.

As the saying goes, no pain, no gain. Investing time now to understand your credit report and credit score will pay big dividends throughout your life.

Here’s What You Need to Know

- The big three credit bureaus primarily focus on what you owe and your repayment history.

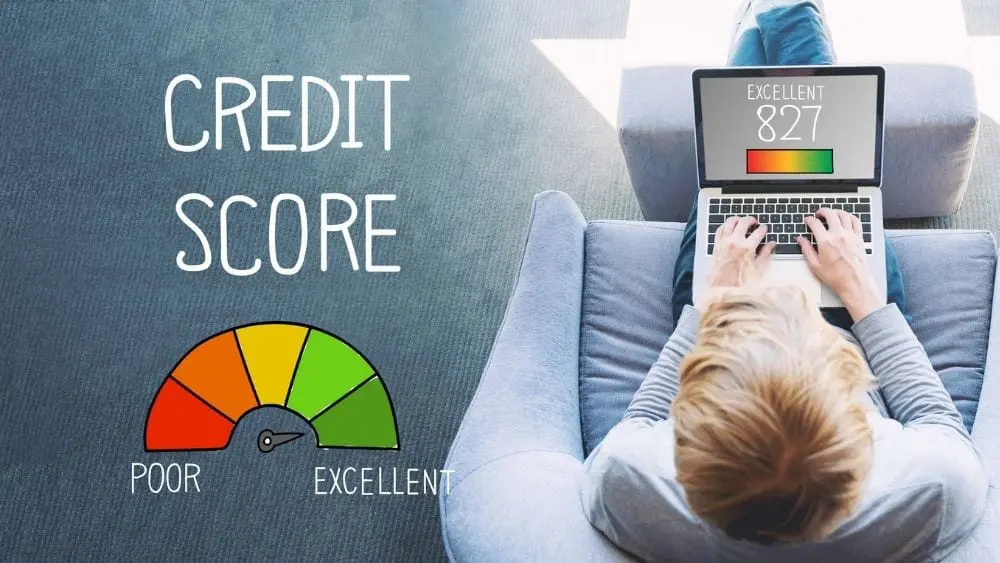

- The most commonly used credit score — also referred to as a FICO score — has a range from 300 to 850.

- Standards can change — and in some cases, have increased for mortgage lenders — as to what’s considered a good credit score

- There’s consensus among experts that 720 is a good score. 740 or higher will typically earn you the lowest interest rates and the best terms.

- Your score helps businesses predict the odds that you’ll go 90 days past due (or default) in the next two years on money that they lend you.

Your FICO Score is Based on 5 Factors:

- Your payment history: 35% of your score.

- Amount of debt you owe: 30% of your score.

- Length of your credit history (generally, longer is better) 15% of your score.

- Amount of new credit you request (too many request for credit, especially in a relatively short period of time is a negative): 10% of your score.

- Types of credit you use: 10% of your score.

Lenders for mortgages, auto loans and credit cards use your score to help understand your ability to pay debt, based on your past payment history. Some newer credit models factor in your income and job history. However, the old saying remains true: The best predictor of future behavior (in this case, paying bills on time) is past behavior.

You may be thinking, it feels like credit scoring is all about rating or even judging me. While there’s an element of truth to that, credit scores benefit each of us as consumers, in important ways:

How to Check Your Credit

- Consumers are entitled to one free credit report every 12 months.

- The three credit bureaus support a website, AnnualCreditReport.com, for that purpose. Use that site. Be wary of others.

- Your credit report will contain detailed information. You should look for errors and correct them.

- Your actual credit score may cost a nominal fee, such as $10, but it’s a worthwhile investment.

Steps You Can Take to Improve Your Credit Score Over Time

- Pay your bills on time.

- Reduce your debt.

- Find and correct any errors in your credit report.

- If you have bad debt, pay it off and ask the debt be marked as paid on your credit report.

- Be patient. None of these steps are instantaneous. However, experts agree that they will work over time.

Now that you understand your credit score, perhaps you’d like to discuss your SAT score, cholesterol level or weight? Ah, thought not! However, with your new credit score knowledge and the steps above, odds are good you can get the new home, car or job you desire, without a credit score standing in your way.

What Lighting is Best for Each Room in Your New Home?

What Lighting is Best for Each Room in Your New Home?